On October 19, 2017, the Internal Revenue Service (IRS) announced via Revenue Procedure 2017-58 the penalties under the Internal Revenue Code (IRC) for failure to file correct Information Returns, such as Forms W-2, 1099 and 1095-C, by the due date, and failure to furnish correct Information Returns to employees and other recipients by the required due date.

Background

Every employer engaged in a trade or business that makes payments for the year for services performed by an employee must file a Form W-2 for each employee from whom income, Social Security or Medicare tax was withheld, and furnish the Form W-2 to their employees.

Applicable Large Employers (ALEs), generally those that employed at least 50 full-time employees (including full-time-equivalent employees) during the preceding calendar year, must file and furnish Forms 1095-C to employees to report whether they offer their full-time employees and any dependents the opportunity to enroll in minimum essential coverage (MEC) under an eligible employer-sponsored plan.

The IRS administers statutory penalties associated with these reporting requirements under Sections 6721 and 6722 of the IRC. Penalty amounts are indexed and may change annually.

Employers must mail or electronically file 2017 Form(s) W-2 and Form W-3 with the Social Security Administration (SSA) by January 31, 2018. Employers must electronically file if required to file 250 or more Forms W-2 or W-2c. Employees must be furnished with their Forms W-2 by January 31.

ALEs must file 2017 Forms 1094-C and 1095-C with the IRS by February 28, 2018 if filing in paper format or by April 2, 2018 if filing electronically. Electronic filing is required for 250 or more Forms 1095-C. Employees must be furnished with Forms 1095-C by January 31, 2018.

Filing Penalties

If an employer fails to file a correct Information Return by the due date and cannot show reasonable cause, the employer may be subject to a penalty as provided under IRC Section 6721. The penalty applies where an employer:

- Fails to file timely.

- Fails to include all information required to be shown.

- Includes incorrect information.

- Files on paper forms when required to electronically file.

- Reports an incorrect tax identification number; i.e., Social Security Number or Employer Identification Number.

- Fails to report a tax identification number.

- Fails to file paper forms that are machine readable.

The amount of the penalty is based on when a correct form has been filed.

Furnish Form(s) to Employees

Generally, employers must furnish Copies B, C, and 2 of Form W-2 to employees by January 31 following the tax year of January 1 through December 31. You will meet the “furnish” requirement if the form is properly addressed and mailed on or before the due date. If employment ends before December 31, employers may furnish copies to the employee at any time after employment ends, but no later than January 31.

Generally, Forms 1095-C must be furnished to employees by January 31 for coverage offered the previous calendar year.

Furnishing Penalties

If an employer fails to provide correct Information Returns (Forms W-2 or 1095-C) to its employees and cannot show reasonable cause, the employer may be subject to a penalty as provided under IRC Section 6722. The penalty applies when an employer:

- Fails to provide the statement by January 31, as required.

- Fails to include all information required to be shown on the form.

- Includes incorrect information on the form.

The amount of the penalty is based on when the employer furnishes the correct form.

Note: The penalty under IRC Section 6722 is an additional penalty to that applied under IRC Section 6721 and is applied in the same manner, and with the same amounts. In other words, both penalties may apply; e.g., if an employer neither furnished a form as required nor filed a form as required. Consequently, the amounts below could be doubled.

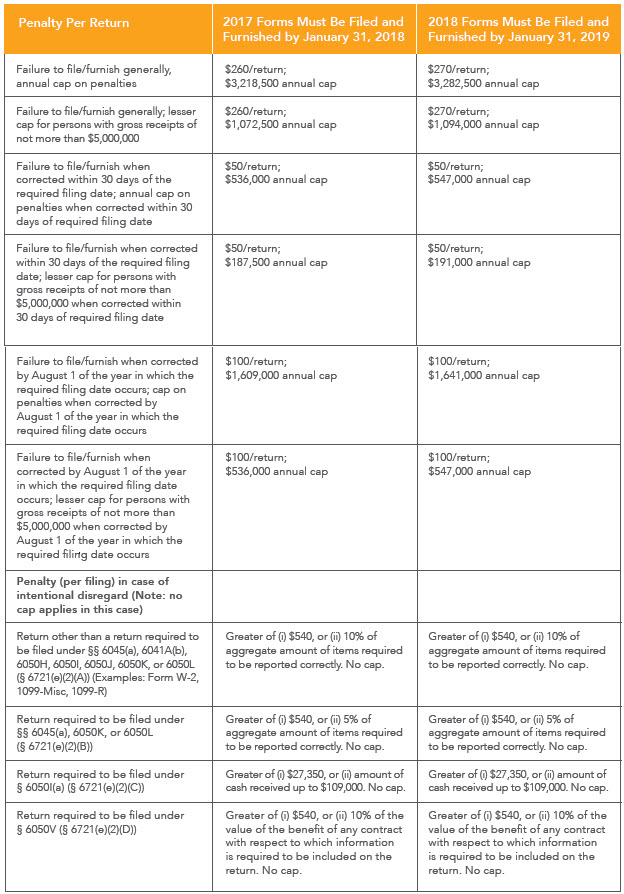

Revenue Procedure 2017-58 modifies the penalties under IRC Sections 6721 and 6722 for tax year 2018 as follows.

Note: Reduced penalties may be applicable for small employers, as defined (generally those with average annual gross receipts for the most recent three years of under $5,000,000). See the Revenue Procedure for details.

To view the IRS Revenue Procedure 2017-58 in its entirety, please visit https://www.irs.gov/pub/irs-drop/rp-17-58.pdf